Kateryna Hronska & Kamran Zamanian, Senior Research Analyst & CEO at iData Research03.20.24

An arthroscope is a compact tube inserted through small incisions, equipped with lenses, a miniature video camera, and a light source for visualizing, diagnosing, and treating joint-related issues. Advancements in arthroscopic technology enable surgeons to examine and resolve joint issues without the necessity for extensive open surgery.

Approximately 11 million arthroscopic surgeries were performed worldwide in 2022.1 Every year, this number increases due to the increasing prevalence of joint-related conditions associated with the aging population, preference for minimally invasive procedures, and soft tissue injuries.

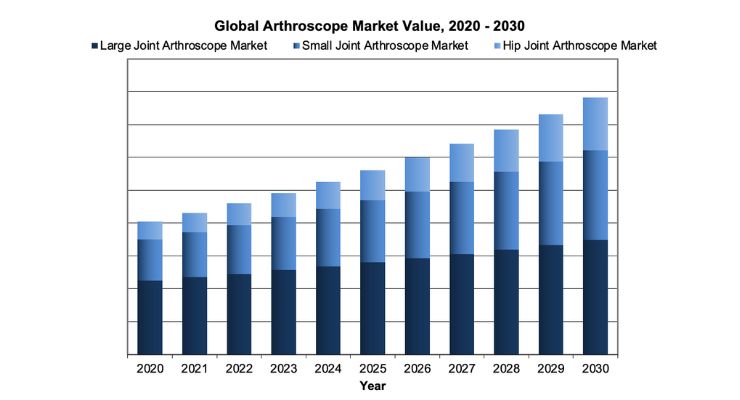

The arthroscopes can be divided into three main categories based on their design, size, and capabilities: large joint arthroscopes, small joint arthroscopes, and hip joint arthroscopes. In 2023, the predominant segment in the arthroscope market was the large joint arthroscope segment, representing a majority share.

This type of arthroscope is mainly used for shoulder and knee arthroscopy, as they have a larger diameter. The large joint arthroscope market is expected to be the slowest-growing market over the forecast period. The large joint arthroscopy market may experience saturation, particularly in regions with high adoption rates. The small joint arthroscope was the second-largest, followed by the hip joint arthroscope market. Small joint arthroscopes have a smaller diameter and therefore are typically used for wrist, elbow, and ankle arthroscopy.

As per the “Global Arthroscope Market Value, 2020-2030” chart above, the large arthroscope market comprised more than half of the total arthroscope market based on the 2023 market value. However, over the forecast period, the large arthroscope’s market share is expected to decline over the forecast period as growth in both the small joint and hip joint markets outpace that of the large joint market.

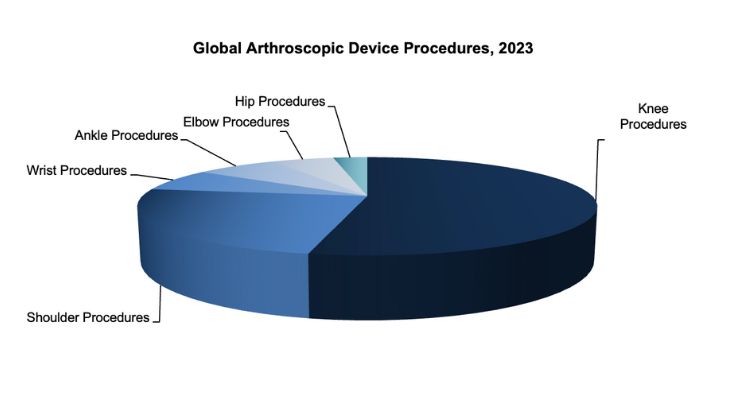

In 2023, knee procedures dominated the arthroscopic landscape, constituting more than half of the total procedures and standing out as the most developed indications within the market as observed in the chart below. Following closely, shoulder procedures secured the second position, comprising nearly a quarter of the total procedures conducted. Conversely, wrist, ankle, and elbow procedures collectively contributed to less than 20% of the global arthroscopies in 2023. Notably, wrist procedures emerged as the predominant small joint arthroscopic procedure, narrowly surpassing ankle procedures in frequency. Despite being a segment with anticipated steady growth in the forecast period, hip arthroscopy retained a relatively modest share of the total arthroscopic procedures in 2022.

Projections suggest a continued upward trajectory for hip procedures; however, even with this robust forecasted growth, hip procedures are expected to maintain a comparatively small proportion of the total arthroscopic procedures in the foreseeable future.

This article will discuss the main driving factors for the continued worldwide growth of arthroscopes.

Global Arthroscope Device Procedures, 2023

Other contributing factors to soft tissue injuries involve overuse or repetitive stress, particularly through engaging in repetitive motions or excessive use of specific muscles or joints. This is frequently observed in activities such as sports, manual labor, or extended periods of typing.

The escalating incidence of soft tissue injuries significantly influences the trajectory of the arthroscopic market. Arthroscopy, distinguished by its minimally invasive methodology, assumes a pivotal role in both the diagnosis and treatment of diverse soft tissue injuries. With heightened awareness and improved diagnostic capabilities for these injuries, there is a corresponding surge in demand for arthroscopic procedures. The market's expansion is propelled by continuous advancements in arthroscopic technology, the broadening spectrum of applications for arthroscopy, and an increasing aging population that is particularly vulnerable to soft tissue injuries.

This shift significantly impacts the arthroscopic market, with arthroscopy aligning well with the preference for less invasive techniques. As more patients and healthcare providers favor procedures with reduced invasiveness and quicker recovery, the demand for arthroscopic procedures rises. The arthroscopic market experiences growth due to the increasing number of surgeries conducted using minimally invasive approaches, supported by continuous innovations in arthroscopic technology, enhancing its appeal in the medical community.

Reference

1. iData Research Inc. Global Arthroscopic Device Market – 2023. Published 2024. Accessed, 2024.

Kateryna Hronska is a senior research analyst at iData Research. She works on research projects regarding the medical device industry, publishing the Global Arthroscopic Device research report.

Kamran Zamanian, Ph.D., is CEO and founding partner of iData Research. He has spent over 20 years working in the market research industry with a dedication to the study of medical devices used in the health of patients all over the globe.

Approximately 11 million arthroscopic surgeries were performed worldwide in 2022.1 Every year, this number increases due to the increasing prevalence of joint-related conditions associated with the aging population, preference for minimally invasive procedures, and soft tissue injuries.

The arthroscopes can be divided into three main categories based on their design, size, and capabilities: large joint arthroscopes, small joint arthroscopes, and hip joint arthroscopes. In 2023, the predominant segment in the arthroscope market was the large joint arthroscope segment, representing a majority share.

This type of arthroscope is mainly used for shoulder and knee arthroscopy, as they have a larger diameter. The large joint arthroscope market is expected to be the slowest-growing market over the forecast period. The large joint arthroscopy market may experience saturation, particularly in regions with high adoption rates. The small joint arthroscope was the second-largest, followed by the hip joint arthroscope market. Small joint arthroscopes have a smaller diameter and therefore are typically used for wrist, elbow, and ankle arthroscopy.

As per the “Global Arthroscope Market Value, 2020-2030” chart above, the large arthroscope market comprised more than half of the total arthroscope market based on the 2023 market value. However, over the forecast period, the large arthroscope’s market share is expected to decline over the forecast period as growth in both the small joint and hip joint markets outpace that of the large joint market.

In 2023, knee procedures dominated the arthroscopic landscape, constituting more than half of the total procedures and standing out as the most developed indications within the market as observed in the chart below. Following closely, shoulder procedures secured the second position, comprising nearly a quarter of the total procedures conducted. Conversely, wrist, ankle, and elbow procedures collectively contributed to less than 20% of the global arthroscopies in 2023. Notably, wrist procedures emerged as the predominant small joint arthroscopic procedure, narrowly surpassing ankle procedures in frequency. Despite being a segment with anticipated steady growth in the forecast period, hip arthroscopy retained a relatively modest share of the total arthroscopic procedures in 2022.

Projections suggest a continued upward trajectory for hip procedures; however, even with this robust forecasted growth, hip procedures are expected to maintain a comparatively small proportion of the total arthroscopic procedures in the foreseeable future.

This article will discuss the main driving factors for the continued worldwide growth of arthroscopes.

Global Arthroscope Device Procedures, 2023

Demographic Factors

The increasing aging population worldwide plays a crucial role in the growing demand for and the advancement of the field of arthroscopy. With aging populations, there is a higher incidence rate of musculoskeletal disorders and joint-related problems, often requiring medical attention. Arthroscopy, a minimally invasive surgical method utilized for diagnosing and treating joint conditions, becomes especially pertinent in meeting the healthcare requirements of an aging demographic. One such reason is the increased incidence of degenerative joint conditions, notably osteoarthritis. With advancing age, joints undergo increased wear and tear, potentially leading to medical conditions requiring medical intervention. Arthroscopy provides a minimally invasive method for both diagnosis and treatment of these joint disorders.Soft Tissue Injuries

Soft tissue injuries refer to damage and trauma that impact the muscles, tendons, ligaments, or other connective tissues in the body. These injuries can arise from diverse causes and may span from mild strains to severe tears. Examples of soft tissue injuries include sprains, strains, contusions, and tendinitis. A prevalent means of incurring such injuries is through trauma, particularly direct impact or force on the soft tissues, as seen in falls, collisions, or accidents.Other contributing factors to soft tissue injuries involve overuse or repetitive stress, particularly through engaging in repetitive motions or excessive use of specific muscles or joints. This is frequently observed in activities such as sports, manual labor, or extended periods of typing.

The escalating incidence of soft tissue injuries significantly influences the trajectory of the arthroscopic market. Arthroscopy, distinguished by its minimally invasive methodology, assumes a pivotal role in both the diagnosis and treatment of diverse soft tissue injuries. With heightened awareness and improved diagnostic capabilities for these injuries, there is a corresponding surge in demand for arthroscopic procedures. The market's expansion is propelled by continuous advancements in arthroscopic technology, the broadening spectrum of applications for arthroscopy, and an increasing aging population that is particularly vulnerable to soft tissue injuries.

Preference for Minimally Invasive Procedures

Minimally invasive procedures present a lot of advantages when compared with traditional open surgeries. Noteworthy benefits include smaller incisions, minimal trauma to adjacent tissues, and minimal scarring. Furthermore, individuals undergoing minimally invasive surgeries frequently enjoy faster recovery periods in contrast to traditional procedures, facilitating a prompt return to routine activities. A pivotal factor contributing to the significance of this technique lies in its capacity to significantly diminish the risk of postoperative infections, owing to the reduction in exposure to external contaminants through smaller incisions. The global trend toward minimally invasive procedures is steadily rising, driven by factors like advancements in medical technology, enhanced surgeon expertise, and increased awareness of their benefits.This shift significantly impacts the arthroscopic market, with arthroscopy aligning well with the preference for less invasive techniques. As more patients and healthcare providers favor procedures with reduced invasiveness and quicker recovery, the demand for arthroscopic procedures rises. The arthroscopic market experiences growth due to the increasing number of surgeries conducted using minimally invasive approaches, supported by continuous innovations in arthroscopic technology, enhancing its appeal in the medical community.

Closing points

The global arthroscopic lens market has been evolving and growing dramatically in the past, and it is expected to maintain growth as the needs of the population increase. With the high cost of most devices, North America and Western Europe represent the highest percentage of the total market. Moreso, arthroscope devices are slowly becoming more prevalent across the globe. Smith & Nephew remains the leading company in the market worldwide.Reference

1. iData Research Inc. Global Arthroscopic Device Market – 2023. Published 2024. Accessed, 2024.

Kateryna Hronska is a senior research analyst at iData Research. She works on research projects regarding the medical device industry, publishing the Global Arthroscopic Device research report.

Kamran Zamanian, Ph.D., is CEO and founding partner of iData Research. He has spent over 20 years working in the market research industry with a dedication to the study of medical devices used in the health of patients all over the globe.